WASHINGTON (AP) — The countdown toward a possible U.S. government default is in the offing — with frictions between President Joe Biden and House Republicans raising alarms about whether the U.S. can sidestep a potential economic crisis.

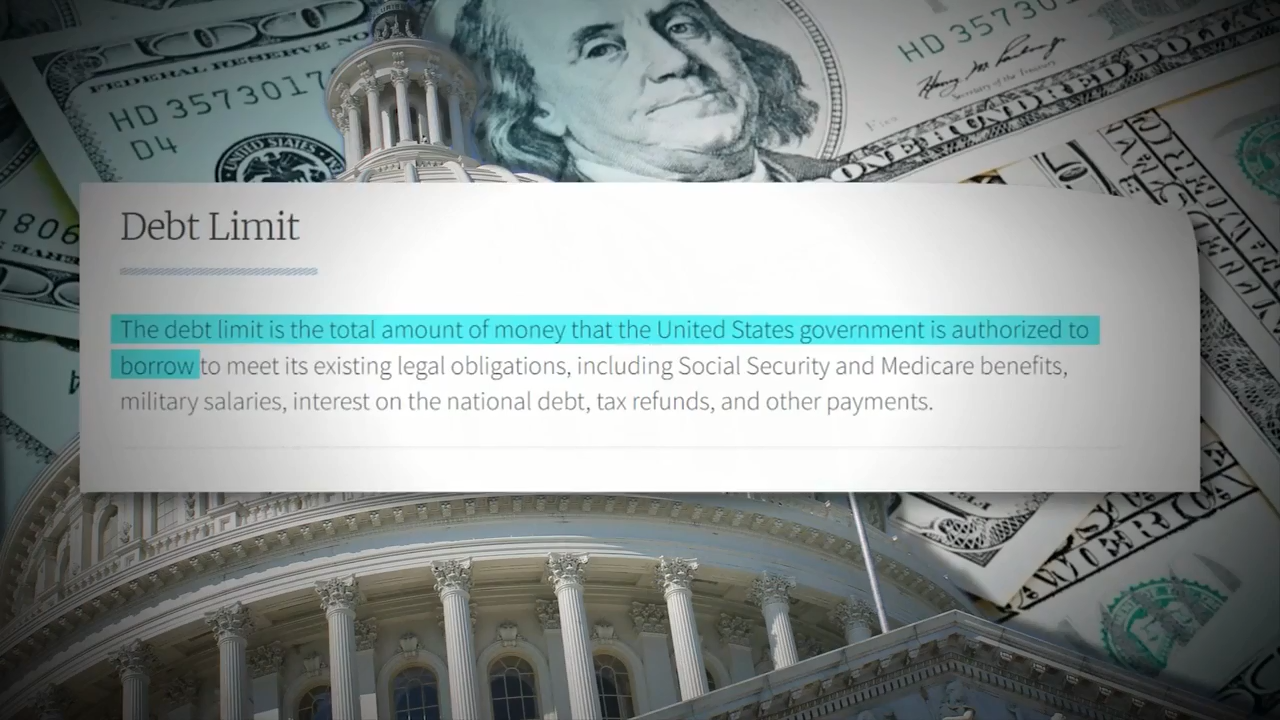

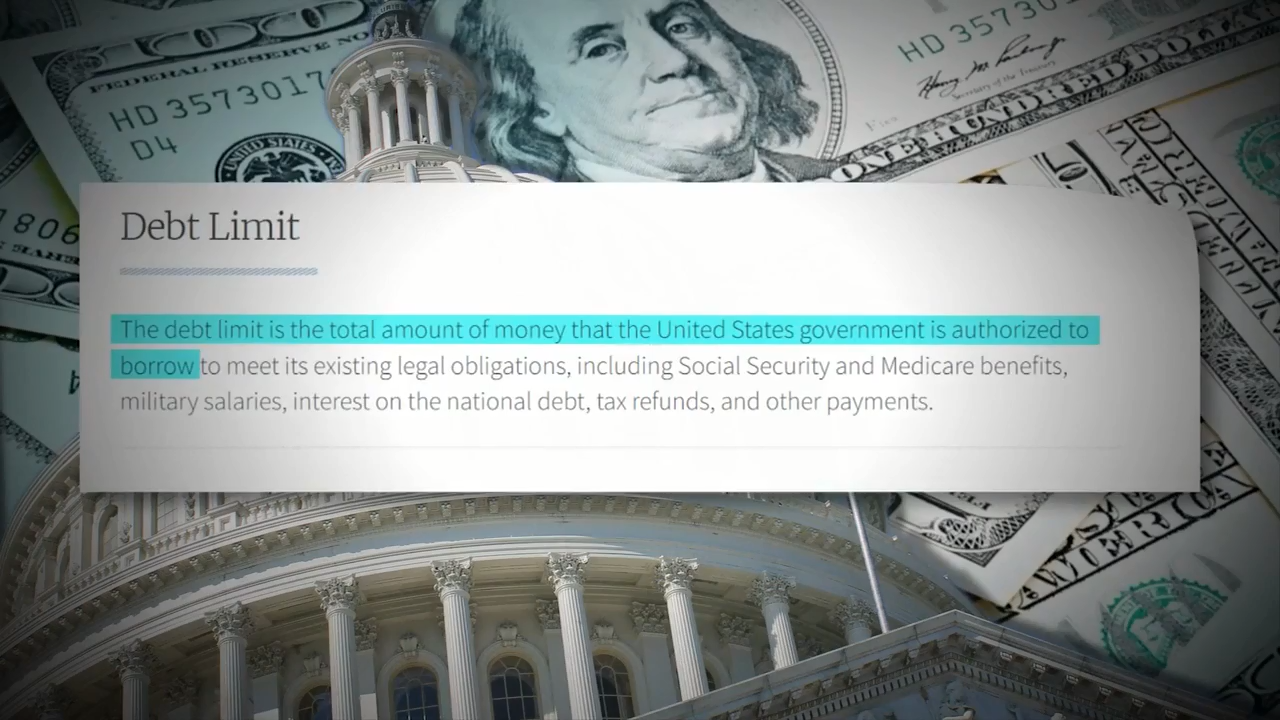

The Treasury Department projects that the federal government will on Thursday reach its legal borrowing capacity of $38.381 trillion, an artificially imposed cap that lawmakers have increased roughly 80 times since the 1960s. Markets so far remain calm, as the government can temporarily rely on accounting tweaks to stay open, meaning that any threats to the economy are several months away. Even many worried analysts assume there will be a deal.

But this particular moment seems more fraught than past brushes with the debt limit because of the broad differences between Biden and new House Speaker Kevin McCarthy, who presides over a restive Republican caucus.

Those differences increase the risk that the government could default on its obligations for political reasons, a problem that could rattle financial markets and — if not resolved — plunge the world’s largest economy into a wholly preventable recession.

The pair have several months to forge a deal, as the Treasury Department imposes “extraordinary measures” to keep the government operating until at least June. But years of intensifying partisan hostility have led to a conflicting set of demands that jeopardize the ability of the U.S. lawmakers to work together on a basic duty.

Biden insists on a clean increase to the debt limit so that existing financial commitments can be sustained, refusing to even start talks with Republicans. McCarthy is calling for negotiations that he believes will lead to spending cuts. It’s unclear how much he wants to trim and if his fellow Republicans would support any deal after a testy start to the new Congress that required 15 rounds of voting to elect McCarthy speaker.

Asked twice Wednesday if there was evidence that House Republicans can ensure that the government will avert a default, White House press secretary Karine Jean-Pierre said it’s their “constitutional responsibility” to protect the full faith and credit of the United States. She did not say whether the White House saw signs at this stage that a default was off the table.

“We’re just not going to negotiate that,” Jean-Pierre said. “They should feel the responsibility.”

For his part, McCarthy said Biden needs to recognize the political realities that come with a divided government. He equates the debt ceiling to a credit card limit and calls for a level of fiscal restraint that did not occur under President Donald Trump, a Republican who in 2019 signed a bipartisan suspension of the debt ceiling.

“Why create a crisis over this?” McCarthy said this week. “I mean, we’ve got a Republican House, a Democratic Senate. We’ve got the president there. I think it’s arrogance to say, ‘Oh, we’re not going to negotiate about pretty much anything’ and especially when it comes to funding.”

Any deal would also need to pass the Democratic Senate. Many Democratic lawmakers are skeptical about the ability to work with Republicans aligned with the “Make America Great Again” movement started by Trump. The MAGA movement has claimed that the 2020 election lost by Trump was rigged, a falsehood that contributed to the Jan. 6, 2021, insurrection at the U.S. Capitol.

“There should be no political brinkmanship with the debt limit,” said Senate Majority Leader Chuck Schumer, D-N.Y. “It’s reckless for Speaker McCarthy and MAGA Republicans to try and use the full faith and credit of the United States as a political bargaining chip.”

In order to keep the government open, the Treasury Department on Thursday was introducing a series of accounting maneuvers known as “extraordinary measures.” These measures put a hold on contributions and investment redemptions for government workers’ retirement and health care funds, giving the government enough financial space to handle its day-to-day expenses until roughly June.

What happens if these measures are exhausted without a deal to raise the debt limit is unknown. A prolonged default could be devastating, with crashing markets and panic-driven layoffs if confidence evaporated in a cornerstone of the global economy, the U.S. Treasury note.

Analysts at Bank of America cautioned in a Friday report that “there is a high degree of uncertainty about the speed and magnitude of the damage the U.S. economy would incur.” The underlying challenge is that the government would have to balance its books on a daily basis if it lacks the ability to issue debt. If the government cannot issue debt, it would have to impose cuts equal in size on an annual basis to 5% of the total U.S. economy. But the analysts say their baseline case is that the U.S. avoids default.

Still, if past debt ceiling showdowns such as the one that occurred in 2011 are any guide, Washington may be in a nervous state of suspended animation with little progress until the “X-date,” the deadline when extraordinary measures are depleted. That creates its own set of challenges.

“A deal probably won’t be reached until the last minute, raising the risk that the deadline to lift the ceiling is inadvertently missed,” said Andrew Hunter, senior U.S. economist at Capital Economics.